Home Equity Loans (HELOANs)

Home Equity Loans (HELOANs) are a key growth product. As a closed-end, fixed rate second mortgage, it addresses the issues of decreased refinance volume and record high home equity. Lenders are adjusting HELOAN offerings to meet consumer demand such as increasing limits, adding 30-year terms, and securitizing billions in volume. The market is seeing innovation from both traditional banks and fintech companies as HELOAN growth continues.

-

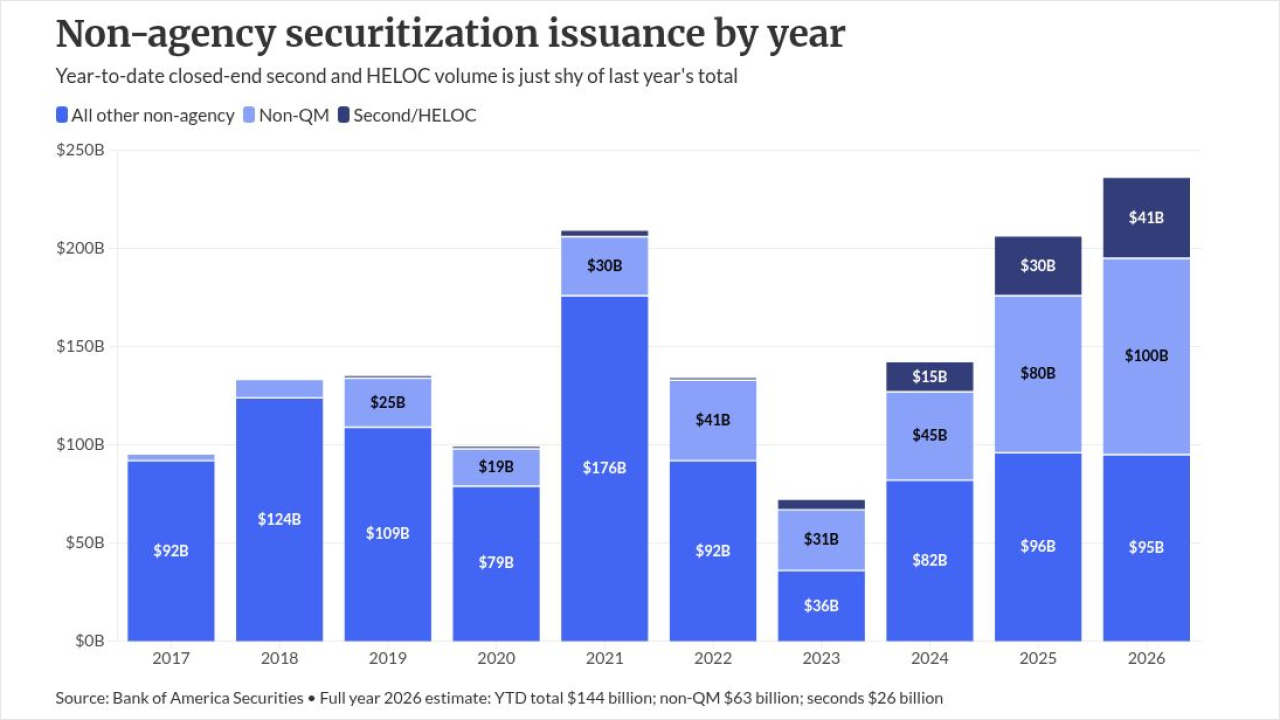

So far this year, the volume of closed-end second and home equity line of credit securitizations is near last year's $29 billion, Bank of America Securities said.

July 27

July 27

-

The share of warehouse lenders offering funding lines and sublimits for seconds has risen to new heights according to a Mortgage Bankers Association survey.

June 9

June 9

-

NAHB's remodeling index finished at its highest mark in a year, with the current industry outlook standing in stark contrast to homebuilder sentiment.

January 16

January 16

-

Home equity is becoming a data-driven asset that demands sharper valuation and analytics as lending options expand, according to Clear Capital's EVP of Strategy and Growth.

December 10 Clear Capital

Clear Capital -

Bank statement loans, a home equity credit card and a blockchain investment product are among the new offerings designed to reach an $11 trillion market.

December 5

-

Billions in home equity sit untapped as second-lien loans struggle to gain traction, writes the chairman of Whalen Global Advisors.

December 2 Whalen Global Advisors LLC

Whalen Global Advisors LLC -

The lender, which reported over $200 million in home equity line of credit volume in the recent quarter, suggests the business can deliver massive scale.

October 21

October 21

The first three months of the year coincide with the start of President Donald Trump's second term in office. Investors are likely to be more interested in banks' outlooks amid swings in tariff policy than the first-quarter results.