-

Self-employed borrowers represent just 23.1% of the pool, and liquid reserves were $858,428 compared with 21.9% and $1 million.

June 8

June 8

-

Certain private-label securities may get a lower risk weighting for bank capital and separately, second liens have new uniform guidelines for TRID.

May 26

May 26

-

Fannie Mae and Freddie Mac should aggressively buy and restructure low-coupon MBS into CMOs rather than holding them, a move that would lower long-term mortgage rates, according to the chairman of Whalen Global Advisors.

April 6 Whalen Global Advisors LLC

Whalen Global Advisors LLC -

Fannie Mae and Freddie Mac have begun placing sizable orders to purchase mortgage-backed securities, stepping into a market roiled by widening bond spreads and a surge in volatility, according to a person with direct knowledge of the matter.

March 22 -

As rising energy prices and growing inflation fears make corporate bonds look increasingly risky, big money managers including State Street and Voya Investment Management have been looking at buying mortgage bonds and other securitized debt instead.

March 22

-

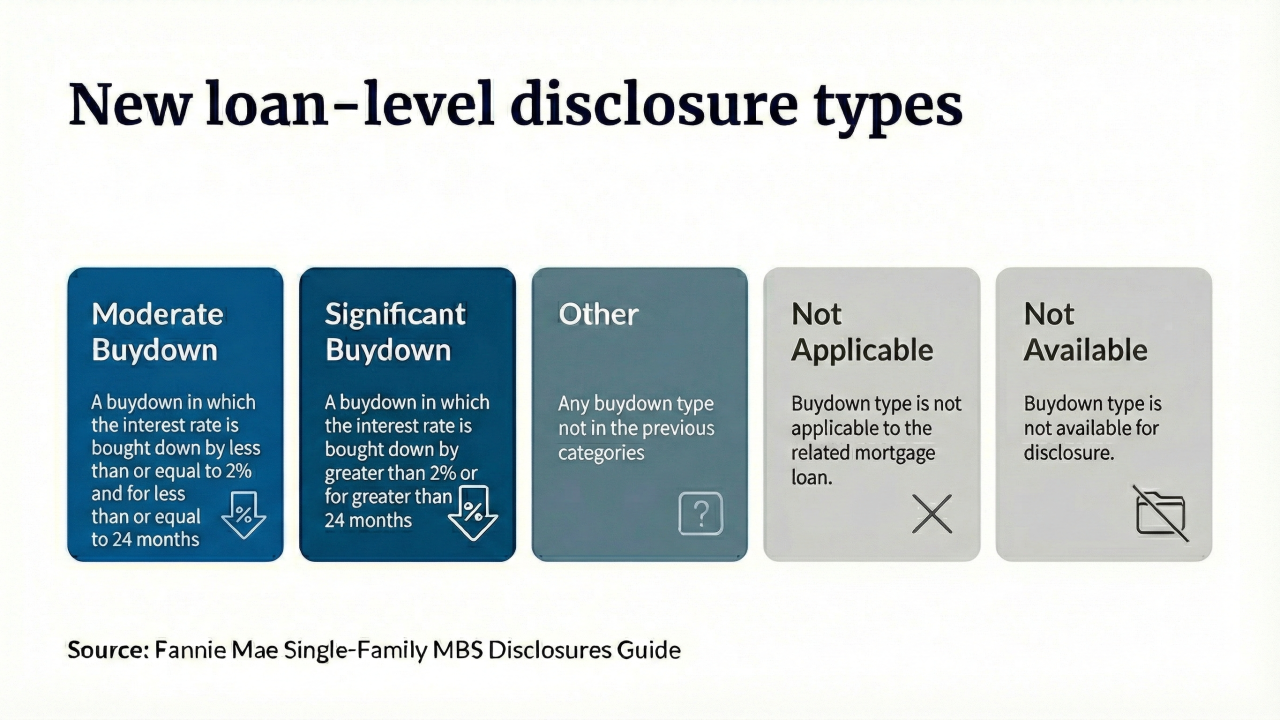

Fannie Mae and Freddie Mac will add loan-level buydown data to MBS this spring, giving investors clearer insight into prepayment risk tied to temporary rate incentives.

February 13

-

The estimated range for net income to common shareholders at the company formerly known as Ocwen rose in part due to a deferred tax asset valuation.

January 26

-

Trump's proposed $200B MBS purchase briefly tightened mortgage spreads, but analysts question the long-term impact on mortgage rates and GSE balance sheets.

January 9

January 9

-

Fannie Mae and Freddie Mac have added billions of dollars of mortgage-backed securities and home loans to their balance sheets in recent months, fueling speculation that they're trying to push down lending rates and boost their profitability ahead of a potential public offering.

December 15

-

Mortgage bonds are on track to deliver their strongest returns in two decades, with the Bloomberg US Mortgage Backed Securities Index having gained 8.35% in 2025 through Friday.

December 2

-

A combination of factors, including the rise of retail investing and sound assets, propelled ETF formation, with at least four issuances over the past year.

November 19

November 19

-

Mortgage groups want GSEs to buy MBS to lower rates, but the Chairman of Whalen Global Advisors writes that the plan is risky, unnecessary, and poorly timed.

October 29Whalen Global Advisors LLC -

FHFA's announcement has investors increasingly concerned about the Bozeman, Montana-based FICO losing both pricing power and a competitive edge.

September 25

-

A possible shift in the composition of the Federal Reserve's portfolio of Treasury holdings could result in the central bank buying nearly $2 trillion of bills over the next two years, enough to absorb nearly all of the Treasury's issuance during that period, according to Bank of America Corp.

August 15

-

-

Alternative asset manager Canyon Partners is committing $250 million to buy new mortgage bonds created by A&D Mortgage LLC, a partnership that will help the mortgage finance company substantially increase the pace of its bond sales.

August 4

-

The funding round will help Button Finance, which leverages AI to underwrite home equity financing, expand its range of products to more borrowers.

May 20

-

Mortgage bonds supported by government-backed companies like Fannie Mae and Freddie Mac were trading slightly wider Monday morning after Moody's Ratings downgraded the US late last week.

May 19

-

A range of investment residential properties, including single-family homes, condominiums and multi-unit properties, will secure the debt.

May 14

-

Agency mortgage backed securities have slipped about 1.1% since the start of April, trailing Treasuries and the broader US bond market.

May 9