-

The deal also includes a 120-day stop advance provision, which prevents it from forwarding any interest and principal on loans that are past 120 days delinquent.

May 22

May 22

-

Secondary market experts are split on whether the Fed's next move will be a rate decrease in 2027 or an increase, as more observers are now thinking.

May 18

May 18

-

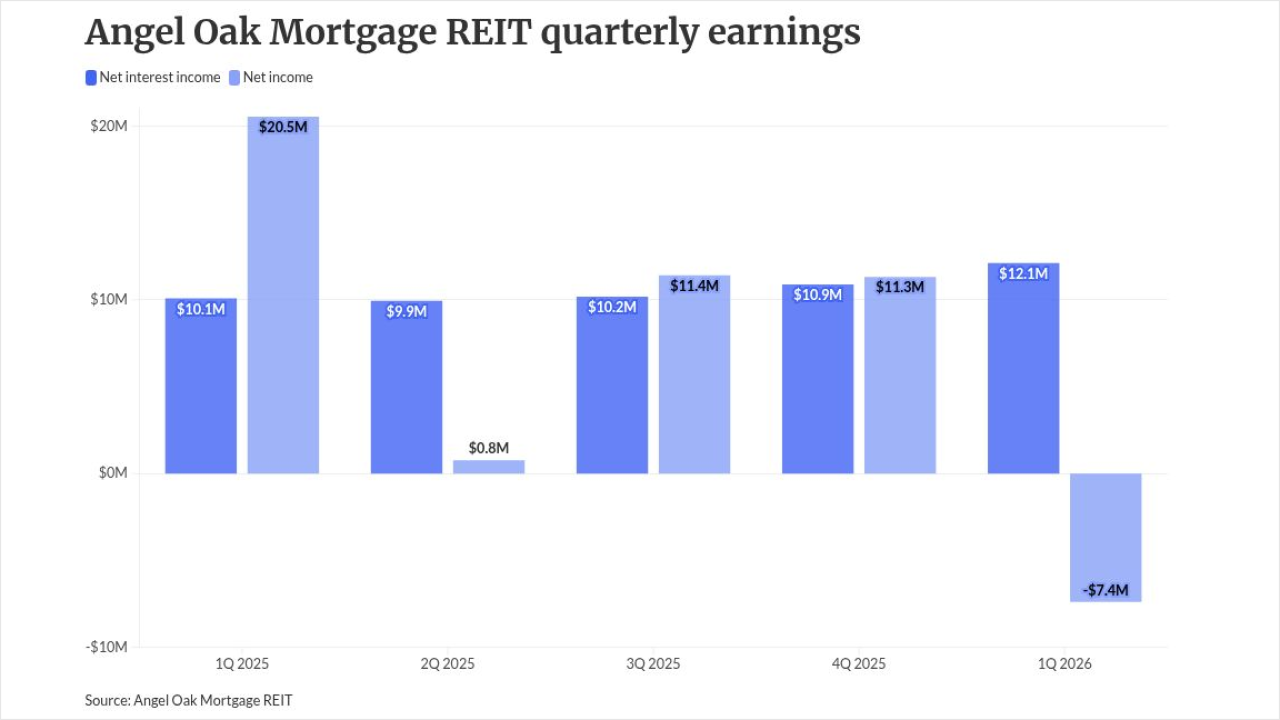

Economic uncertainty weighed on risk appetite, but the current performance of the non-QM market is "durable," Angel Oak leaders said in an earnings call.

May 5

May 5

-

Losses stemming from the 2022 vintage have been offset by excess spread, while cure and roll rates signal caution.

April 6

-

Fannie Mae and Freddie Mac should aggressively buy and restructure low-coupon MBS into CMOs rather than holding them, a move that would lower long-term mortgage rates, according to the chairman of Whalen Global Advisors.

April 6 Whalen Global Advisors LLC

Whalen Global Advisors LLC -

Full documentation was completed on just 17.9% of the pool, Fitch said, while bank statements and debt service coverage ratio (DSCR) account for 17.6% and 28.0%, respectively.

March 31

-

A federal appeals court ruled mortgages in REMIC trusts may qualify as ERISA plan assets, reviving fiduciary duty claims against Onity in a case brought by a union pension fund.

March 30

-

Full documentation was only applied to 2.6% of the underlying pool of mortgages. Debt-to-income, however, was 23.3% when it was applied.

March 26

-

Some 90.3% of the loans have had a clean payment history over the past 12 months, with a 1.3% delinquency rate.

March 25

-

Most of the loans, 57.34%, are for cashout purposes and the entire loan pool are first-liens, and are of modest leverage, with an original cumulative loan-to-value (LTV) ratio of 69.74%.

March 24

-

Fannie Mae and Freddie Mac have begun placing sizable orders to purchase mortgage-backed securities, stepping into a market roiled by widening bond spreads and a surge in volatility, according to a person with direct knowledge of the matter.

March 22 -

As rising energy prices and growing inflation fears make corporate bonds look increasingly risky, big money managers including State Street and Voya Investment Management have been looking at buying mortgage bonds and other securitized debt instead.

March 22

-

RATE 2026-J1 has a seasoned probability of default of 6.4% and 1.3% on the 'AAA' and 'B' rating stress levels, respectively.

March 17

-

FIGRE 2026-HF3 will repay noteholders on a pro rata basis but is subject to a provision that requires the deal to repay noteholders sequentially after a credit event.

March 13

-

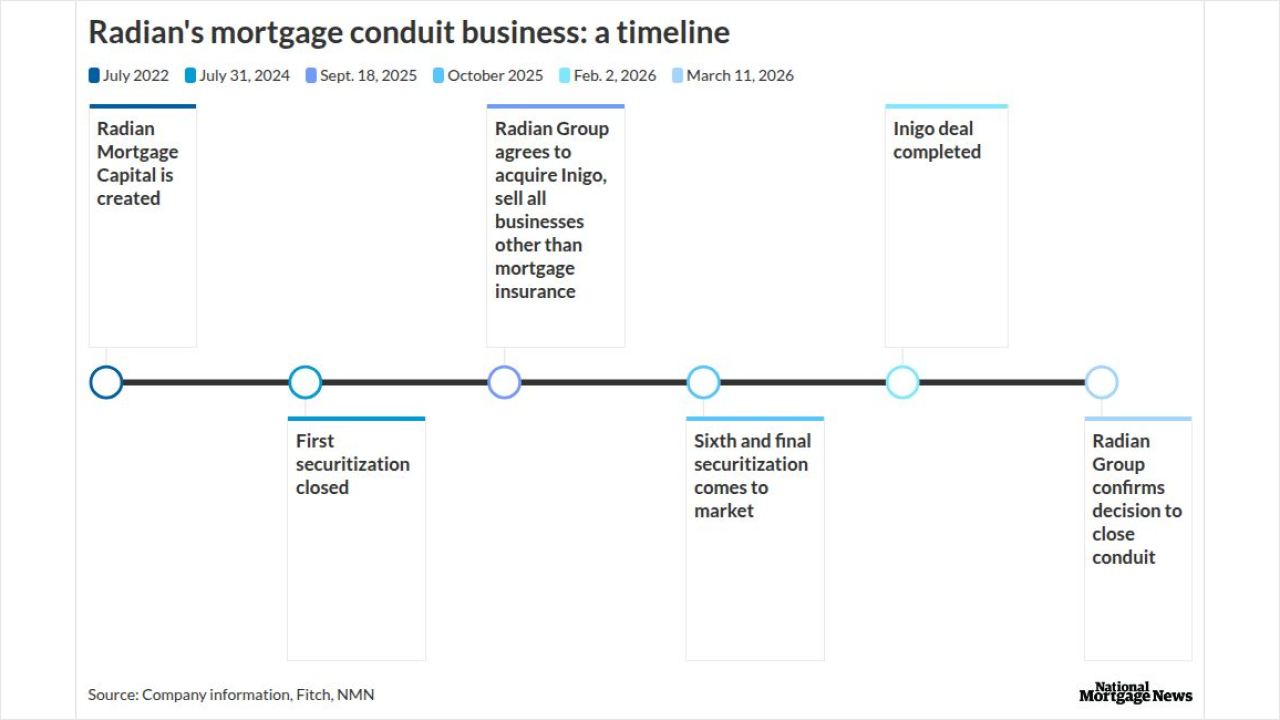

Radian Group was looking to sell the aggregator, along with its title and real estate units, following a business model pivot related to the Inigo buy.

March 11

-

The Mortgage Industry Standards Maintenance Organization is nearing completion on the first of a three-phase Veterans Affairs loan guarantee modernization effort.

March 6

-

The deal benefits from three accounts–a Funding, Expense Reserve and Interest Reserve. The Funding Account will fund draws and purchase additional loans.

March 3

-

Gatti will be based in the firm's Washington, D.C. office, where he focuses on structuring and executing asset-backed securities deals and other structured finance transactions.

February 23

-

GSMBS 2026-PJ2's losses are based on a senior-subordinate, shifting-interest structure and Fitch expects a 10.3% final probability of default in the AAA rating stress.

February 20

-

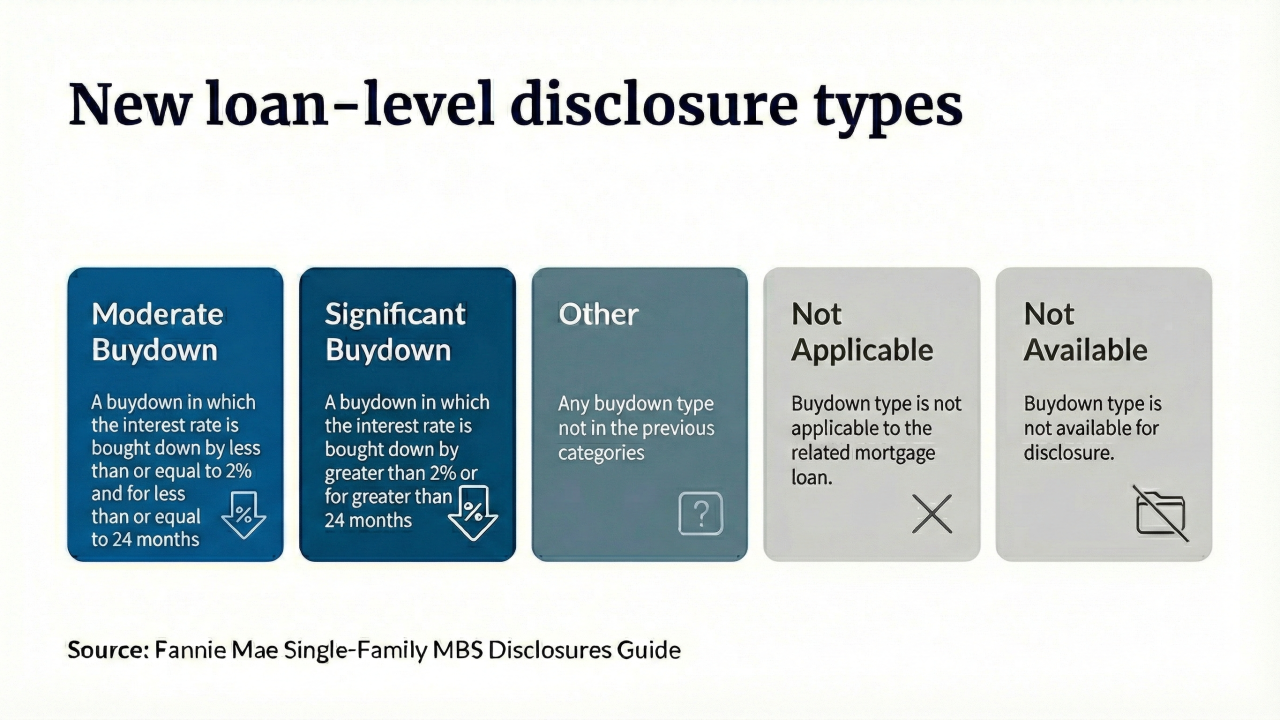

Fannie Mae and Freddie Mac will add loan-level buydown data to MBS this spring, giving investors clearer insight into prepayment risk tied to temporary rate incentives.

February 13

February 13