-

The transaction uses a shifting interest repayment structure, and its lockout that is subject to performance triggers.

November 24

November 24

-

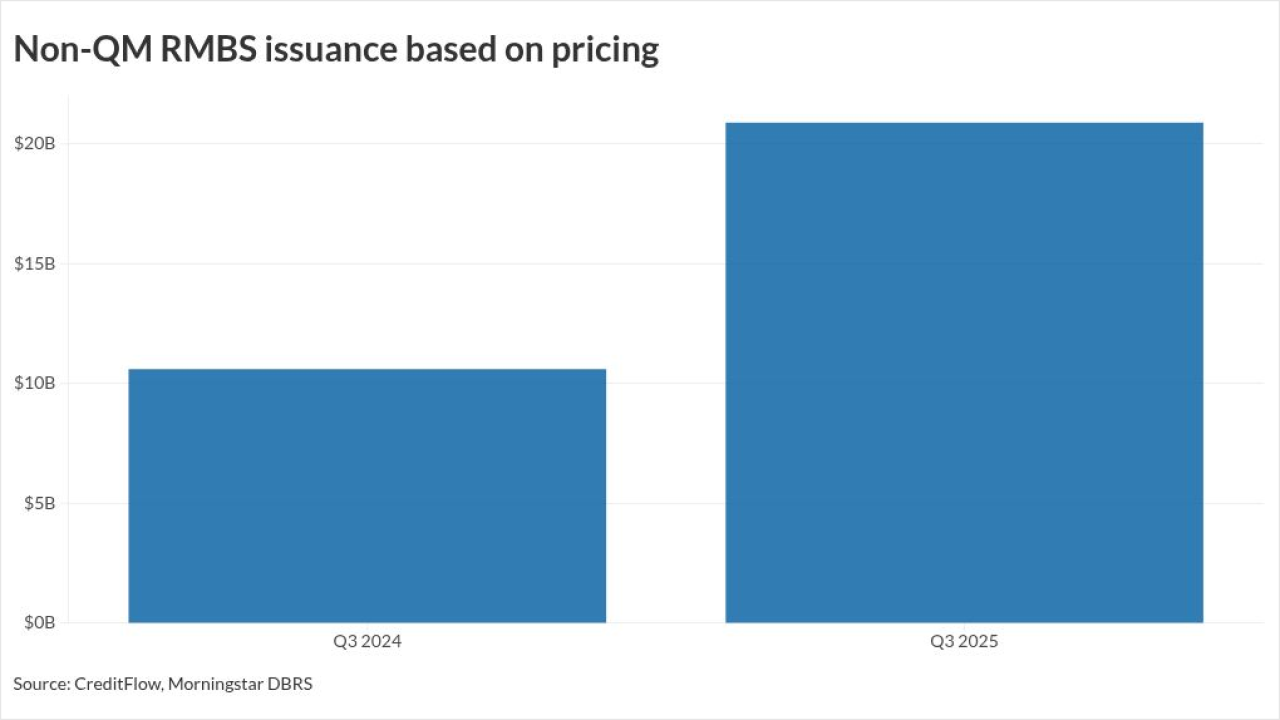

New private-label bonds collateralized by loans made outside the qualified mortgage definition hit highs for the month, quarter and year, CreditFlow data shows.

November 24

November 24

-

A combination of factors, including the rise of retail investing and sound assets, propelled ETF formation, with at least four issuances over the past year.

November 19

November 19

-

The Structured Finance Association is adding its weight to recent support for a Securities and Exchange Commission action that could modernize Reg AB II.

November 18

-

SEMT 2025-12's collateral profile is slightly weaker compared with the prior transaction, with a slightly lower weighted average FICO score.

November 12

-

Second-lien mortgages make up the collateral pool. Those assets normally have a high expected loss severity, but the borrowers appear to be of prime credit quality.

November 11

-

Most of the pool of 1,011 residential mortgages, 69.7%, are considered non-prime mortgages, primarily due to the documentation and styles of underwriting.

November 3

-

Now that quantitative tightening is ending, the debate on who should be the MBS buyer of last resort, Fannie Mae and Freddie Mac, or the Fed, is taking hold

November 3

November 3

-

FFIN 2025-3's average loan balance, $16,366 was lower compared with the 2025-2 deal, when it was $19,993, and the WA interest rate on the current deal is 12.15%, down from 12.56%.

October 30

-

Mortgage groups want GSEs to buy MBS to lower rates, but the Chairman of Whalen Global Advisors writes that the plan is risky, unnecessary, and poorly timed.

October 29 Whalen Global Advisors LLC

Whalen Global Advisors LLC -

Overall, new 60-day-plus delinquencies totaled $2 billion, up from $1.69 billion in August, while maturity defaults accounted for half, or 51% ($1.05 billion) of new delinquencies.

October 20

-

Karsten Giesecke and Michael Karol join Morriello to represent clients such as lenders and private equity funds in transactions including RMBS, CMBS, franchise loans and esoteric assets.

October 17 -

Rithm Capital, a real estate investment trust, is sponsoring the deal, in which property focused investor loans represent 32.60% of the collateral pool.

October 6

-

The NCUA, as liquidating agent for three failed corporate credit unions, sued in 2018 claiming U.S. Bank failed to perform its role as RMBS trustee.

October 6

-

FHFA's announcement has investors increasingly concerned about the Bozeman, Montana-based FICO losing both pricing power and a competitive edge.

September 25

-

Fintech loan provider Knock said the transaction will allow it to accelerate funding for its bridge financing originations, which surged 126% year over year.

August 26

-

Most of the pool, 68.6%, is in the repayment phase, while 19.1% of the loans in the pool are in deferment.

August 18

-

A possible shift in the composition of the Federal Reserve's portfolio of Treasury holdings could result in the central bank buying nearly $2 trillion of bills over the next two years, enough to absorb nearly all of the Treasury's issuance during that period, according to Bank of America Corp.

August 15

-

Delinquencies within the segment eased from the first quarter to the second, but prepayments increased, Morningstar DBRS reported.

August 13

-