-

The RMBS deal expects to pay coupons of 4.53% on the A1A through B4 notes, virtually all the notes in the capital structure.

July 27

July 27

-

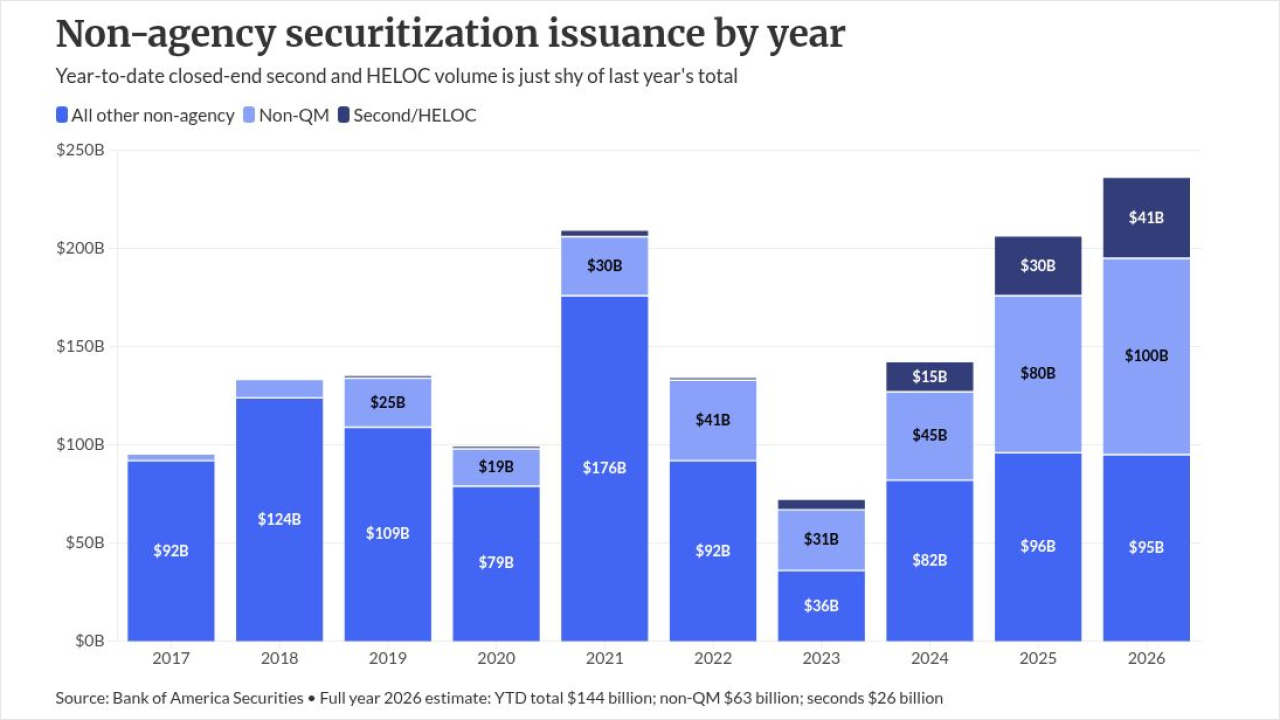

So far this year, the volume of closed-end second and home equity line of credit securitizations is near last year's $29 billion, Bank of America Securities said.

July 27

July 27

-

Lenders are still sending files to their secondary market partners with missing or misplaced documents, affecting how the collateral is viewed and priced.

July 22

-

Almost one third of borrowers in the pool, 26.3%, are self-employed, with a non-zero weighted average (WA) average income of $832,522, and $666,211 in liquid reserves.

July 21

-

Figure Lending originated the HELOCs using the FICO 9 scoring model, which treats medical debt, rental payments and repaid collection accounts differently.

July 7

-

Expected coupons range from 5.66% on the AAA-rated A-1A tranche to 8.52% on the tranche rated B+.

July 1

-

Investment properties are not only in the majority, 56%, but they represent the largest portion of the pool since the AOMT 2025-12 transaction, which priced in November 2025.

June 30

-

Fake jumbo mortgages are helping non-agency securitization growth, but these loans could have higher than expected delinquency rates, an analysis said.

June 29

-

Of the alternative documentation used, bank statements looking back 12-23 months, accounted for 41.6% of that group.

June 29

-

DSCR loans once allowed coverage ratios as low as 0.65, but 2023-24 vintage stress is pushing lenders toward stricter underwriting and interest-only structures.

June 26

-

Foundation had introduced Version 3 of its credit risk model, using the most recent delinquency data, to improve loan performance predictions.

June 24

-

The industry association said total multifamily mortgage debt alone increased by $23 billion, or 1% in Q1, representing a $2.32 trillion increase from Q4 2025.

June 18

-

The A1A through A1-LCF tranches are expected to offer coupons of 5.84%, while mezzanine and subordinate coupons include 6.58% and 6.64%.

June 18

-

Aspire will raise $468.8 million from a pool of 917 residential mortgages, which are primarily fixed-rate.

June 15

-

The deal will bring Kiavi's assets onto Figure's blockchain environment, adding $7 billion in annual volume, and more than $100 million of monthly cash flow onto its blockchain-native warehouse marketplace, Democratized Prime.

June 10

-

The deal includes recently introduced senior first class flow (A-1FCF) and last cash flow (A-1LCF) tranches, which benefit from credit enhancement levels of 24.70%.

June 9

-

Self-employed borrowers represent just 23.1% of the pool, and liquid reserves were $858,428 compared with 21.9% and $1 million.

June 8

-

Second homes account for 10.1% of the underlying collateral pool, the highest ratio seen in pools all year.

June 3

-

The capital structure includes first cash flow and last cash flow notes among the senior classes, and expected coupons include 5.64% on the A1A, A1B, A1FCF, A1LCF and A1 notes.

June 1

-

Certain private-label securities may get a lower risk weighting for bank capital and separately, second liens have new uniform guidelines for TRID.

May 26

May 26