Home Equity Lines of Credit (HELOCs)

Home Equity Lines of Credit (HELOCs) are experiencing a resurgence due to both homeowners having trillions in tappable equity as well as many being locked into low-rate mortgages. Borrowers are seeking liquidity without refinancing. Banks and independent mortgage lenders are responding to this by expanding HELOC products, increasing limits, and embracing new technology and digitization. Current areas of focusing include securitizations gaining momentum, rising fraud threats, and intensifying competition is intensifying. HELOCs have re-emerged as a strategic growth lever for mortgage professionals.

-

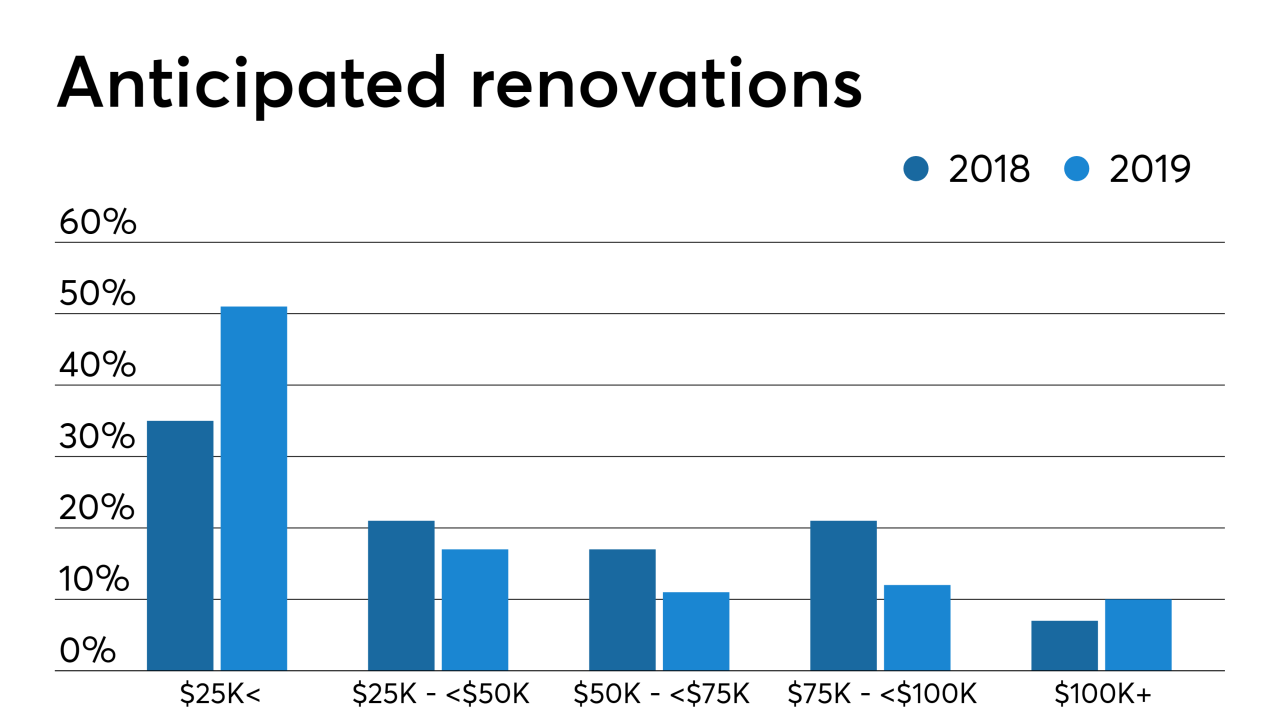

With nearly half of homeowners renovating in the next two years, HELOCs stand as the most likely form of lending sought out by consumers, according to TD Bank.

July 10

July 10

-

Cerberus affiliate FirstKey Mortgage will pool outstanding first- and second-lien loans totaling $277.7 million drawn from 1,732 seasoned and performing HELOCs.

June 14

-

It’s the one consumer loan category where balances continue to fall, and disruption from nimbler fintechs is a big reason why. To win back market share, banks will need to beat the upstarts at their own game.

June 7

June 7

-

The shift to nonbank lenders will put the breaks on non-qualified mortgage and home equity line of credit origination growth.

May 20 Whalen Global Advisors LLC

Whalen Global Advisors LLC -

Live Well Financial, a reverse and traditional mortgage lender that abruptly stopped originating on May 3, will lay off 103 employees, according to a Virginia Employment Commission filing.

May 7

May 7

-

The number of homeowners likely to qualify for a refinance nearly doubled in a single week following the largest mortgage rate decline since the housing bubble burst, according to Black Knight.

April 1

April 1

-

Point, which provides an alternative to traditional home equity lending products, has raised $122 million in new capital from eight investors to expand its reach.

March 20

March 20

The first three months of the year coincide with the start of President Donald Trump's second term in office. Investors are likely to be more interested in banks' outlooks amid swings in tariff policy than the first-quarter results.

- July 16

-