Home Equity Lines of Credit (HELOCs)

Home Equity Lines of Credit (HELOCs) are experiencing a resurgence due to both homeowners having trillions in tappable equity as well as many being locked into low-rate mortgages. Borrowers are seeking liquidity without refinancing. Banks and independent mortgage lenders are responding to this by expanding HELOC products, increasing limits, and embracing new technology and digitization. Current areas of focusing include securitizations gaining momentum, rising fraud threats, and intensifying competition is intensifying. HELOCs have re-emerged as a strategic growth lever for mortgage professionals.

-

The Consumer Financial Protection Bureau seeks to address challenged posed by the sunset of the London interbank offered rate at the end of 2021.

June 4

-

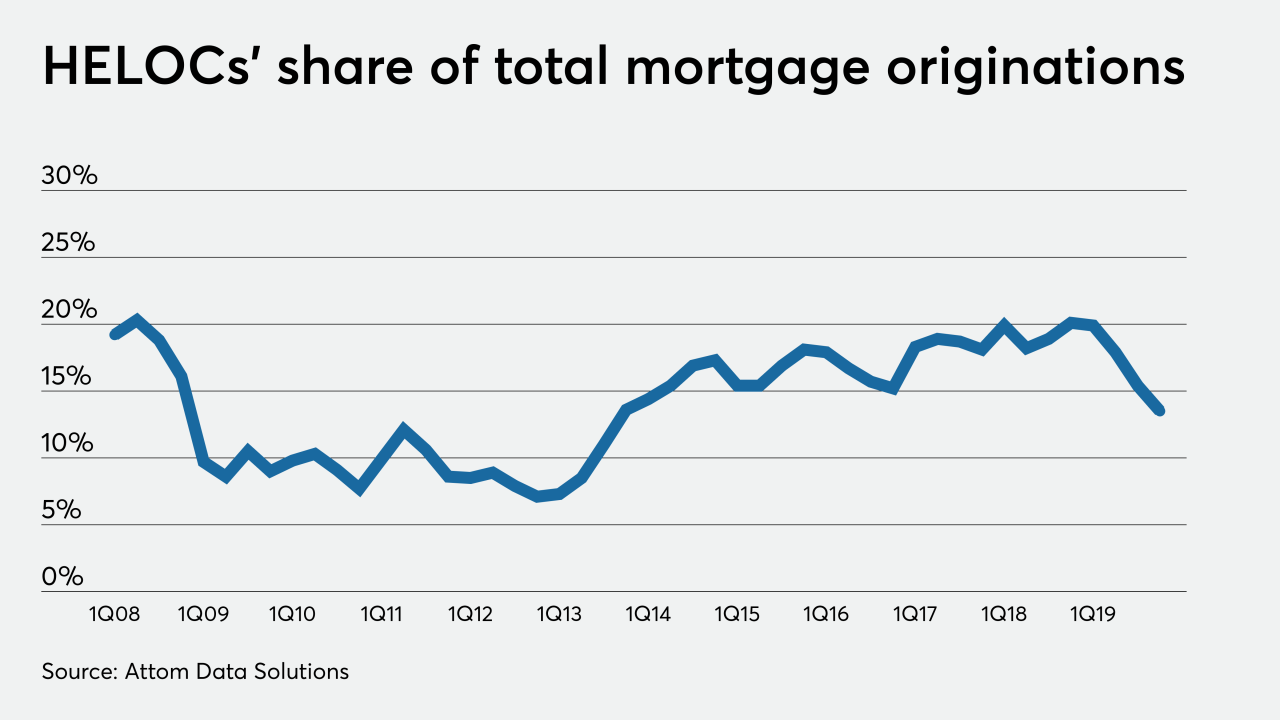

With mortgage rates reaching all-time lows in the opening quarter, refinance originations were up in 97% of housing markets during 1Q, according to Attom Data Solutions.

May 21

May 21

-

Wells Fargo will temporarily stop accepting applications for home equity lines of credit, following a similar move by rival JPMorgan Chase.

April 30

-

Is JPMorgan Chase an outlier or the canary in the coal mine when it comes to home equity lending during the coronavirus spread?

April 28

April 28

-

The nation's largest bank is temporarily reducing its exposure to the mortgage market amid rising unemployment and estimates that home prices could drop by 10%.

April 16

April 16

-

The worsening economy brought on by the coronavirus pandemic has big banks rethinking who they will lend to.

April 2

-

JPMorgan Chase & Co. is shifting workers to handle an expected surge in demand for home loans as the American housing market looks forward to its strongest spring in at least a decade and the coronavirus sends mortgage rates lower.

February 28

The first three months of the year coincide with the start of President Donald Trump's second term in office. Investors are likely to be more interested in banks' outlooks amid swings in tariff policy than the first-quarter results.